Inflation erodes your savings silently. Banks keep most of the available interest for themselves. The numbers are not subtle, they are extraordinary.

€554k Real value of €1m after 20 yrs at 3% inflation | €258k Real value of €1m after 20 yrs at 7% inflation | −74% Purchasing power destroyed in 20 yrs at 7% inflation |

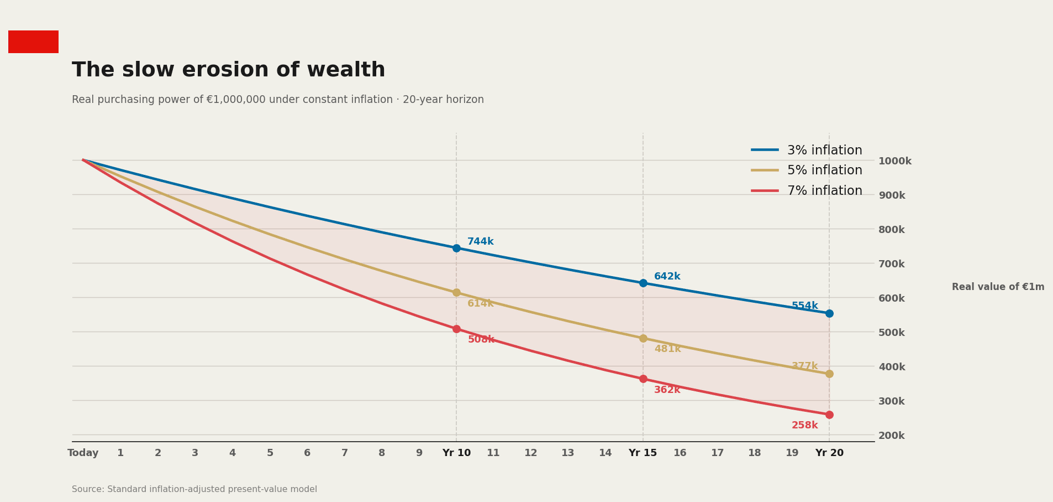

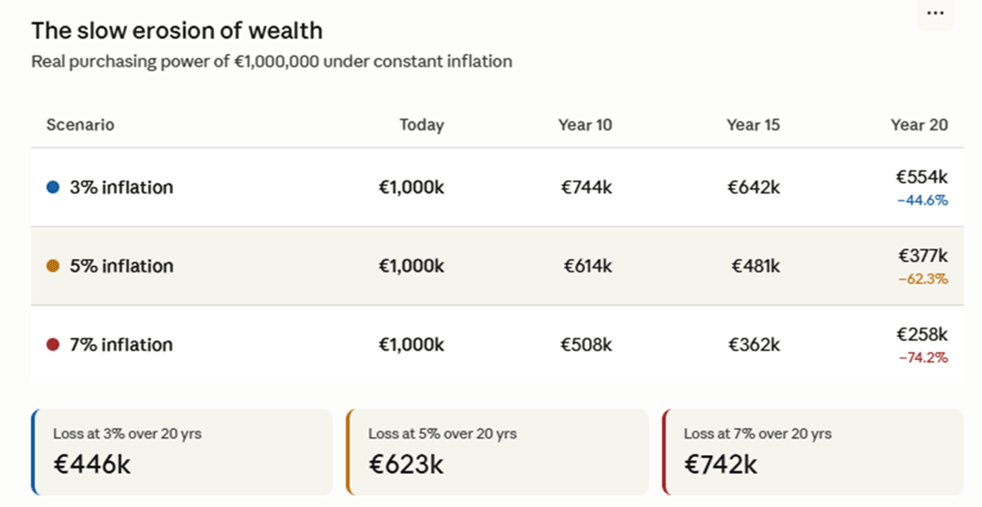

The certain loss: what inflation does to cash

Keeping money in a bank account is not the safe option. It is an option with a mathematically guaranteed negative outcome. At 3% annual inflation, €1 million has the purchasing power of just €554,000 after twenty years. At 7%, a rate seen across southern Europe in 2022–23, barely €258,000 remains. Almost three-quarters of the wealth is gone, consumed not by any bad investment, but by the simple act of doing nothing.

“The greatest risk may be the one disguised as safety. Choosing not to act is not avoiding risk, it is a decision with a precisely calculable, negative outcome.”

Source: Standard inflation-adjusted present-value model. Values in constant euros.

Inflation: the silent thief that steals your savings

What your bank pays vs what it earns

When you place money in a bank account, the bank can use those funds in several ways to generate returns, such as making loans, investing in securities, or simply depositing excess cash with the European Central Bank (ECB). The ECB currently pays banks 2.00% interest on overnight reserves, providing a risk-free return with full daily liquidity and no lock-up period.

In smaller, concentrated markets such as Cyprus and Greece, banks pass on very little of the returns they earn, keeping most of the difference (the “spread”) for themselves. When you borrow, banks pass higher rates on immediately. When you save, they pass them on as slowly as they can.

The table below compares the interest banks earn from the ECB on customer deposits with the rates they pay depositors across the main EU countries.

Annual income on €1,000,000 — by country

What banks earn from the ECB on your deposit vs what they pay you

Country | Deposit rate | Pass-through | You earn / yr | Bank keeps / yr |

ECB (what bank earns) | 2.00% | 100% | €20,000 | — |

Germany | 1.90% | 95% | €19,000 | €1,000 |

Netherlands | 1.80% | 90% | €18,000 | €2,000 |

France | 1.65% | 83% | €16,500 | €3,500 |

Italy | 1.65% | 83% | €16,500 | €3,500 |

Greece | 1.10% | 55% | €11,000 | €9,000 |

Cyprus (best rate, 1yr term) | 0.87% | 44% | €8,700 | €11,300 |

Cyprus (savings account) | 0.00% | 0% | €0 | €20,000 |

Sources: ECB MIR statistics · Central Bank of Cyprus published bank-level data (2025)

Why southern Europe is worst affected

In Cyprus, three banks control 85% of total banking assets. In Greece, four systemic banks dominate similarly. This is not a competitive market, it is an oligopoly. Banks set deposit rates at the minimum required to stop customers leaving. Since choice is limited, and switching is difficult, that minimum is very low.

The same banks charge among the highest lending rates in the eurozone, Cyprus mortgage rates averaged 4.01% in 2025, against a 3.50% eurozone average. In 2013, Cyprus depositors learned the hardest lesson: when the bail-in hit, those with over €100,000 lost money overnight. Cash is not risk-free. It simply carries different risks.

A depositor with €1,000,000 in a Cypriot savings account earns €0 per year. Their bank earns €20,000 from the ECB on that same money — overnight, risk-free. After 3% inflation, the real loss exceeds €30,000 every single year. Silently. Automatically. Without a single investment decision being made.

The Hidden Cost of Inaction

Sometimes, the greatest risk is not investing at all.

Holding cash is frequently mischaracterized as a safe strategy, yet it guarantees exposure to two critical hazards: bank failure and the absolute certainty of inflationary erosion. Cash is the easiest decision to make, and often the most expensive one to live with.

Ultimately, avoiding the market is not a risk-free choice. The true question is not whether you should take risks, but rather which risks you choose to manage consciously, and which ones you accept by default, every day, without realizing it.

Standing still is a guaranteed loss. Doing nothing is not a neutral choice, it is a decision with a cost. The question is not whether you will face risk, but whether you will manage it intentionally or try to ignore it and accept it passively.

Ultimately, the choice between investing your capital and allowing it to slowly melt away may be one of the most consequential financial decisions you ever make. It could mean the difference between retiring with comfort, independence, and peace of mind, or merely scraping by.

“Every other investment might lose money. Cash definitely will.”

Sources

ECB MIR statistics (2025) · Central Bank of Cyprus (Jul–Oct 2025) · Allianz Research (Feb 2026) · CBC research / Avgousti & Michael (Mar 2026) · World Bank Global Financial Development · IMF Working Paper 2024/142. This document is for informational purposes only and does not constitute investment advice. All investments carry risk.

Important Disclaimers: Numbers and illustrations are for educational purposes only and do not represent guarantees of future results. Past performance is not indicative of future returns. This is a marketing communication and does not constitute investment advice. The information and opinions expressed herein are solely those of the author. Investing involves risk - your capital is at risk.