-(1).png)

It seems simple: you’ve built up your wealth, and now it’s time to enjoy it. Just take what you need, right?

But turning your savings into reliable income isn’t as straightforward as it looks. In fact, doing it the wrong way — withdrawing too much, too rigidly, or at the wrong time — could quietly destroy your wealth. One bad strategy can outpace your portfolio, leave you exposed to market shocks, and turn your golden years into a period of stress and scarcity.

Getting it right isn’t just smart — it’s essential.

For many investors, the primary focus is on building a portfolio — accumulating wealth through disciplined saving, diversified investments, and steady compounding. However, once retirement begins or income needs arise, the objective shifts: it’s no longer just about growth, but about preserving that wealth while drawing income from it.

This is where a well-planned withdrawal strategy becomes essential. Without one, even the most carefully constructed portfolio can be eroded by market volatility, inflation, or poor timing. A rigid or poorly timed withdrawal approach can quietly destroy decades of savings, especially when early losses are compounded by withdrawals.

By contrast, implementing a smart, dynamic withdrawal strategy can help maintain income, preserve capital, and reduce stress — even in uncertain market environments.

How Withdrawals Can Hurt Your Portfolio

1. Sequence of Returns Risk

When you withdraw a fixed amount from your portfolio during a market downturn, you’re effectively selling more shares at lower prices. This locks in losses and reduces the portfolio’s ability to recover — a danger known as sequence of returns risk.

Example:

You retire with $1,000,000 and plan to withdraw $50,000 annually.

In Year 1, the market drops 20%, and the portfolio falls to $800,000.

After withdrawing $50,000, you're left with $750,000.

Even if the market rebounds the following year, you're now growing from a smaller base — limiting your recovery.

In contrast, if those same negative returns occurred later in retirement (after several years of growth), the impact would be much less severe.

2. Inflation Can Erode Purchasing Power

Many retirees set a fixed withdrawal amount (e.g., $50,000/year), but inflation steadily reduces its purchasing power.

For example:

$50,000 in today’s dollars would be worth only about $36,800 in 10 years, assuming 3% annual inflation.

Without inflation adjustments, retirees may:

Be forced to cut spending in later years, or

Overspend early, leading to faster depletion.

3. Rigid Withdrawals During Market Volatility

Markets don’t deliver stable returns every year. A fixed withdrawal strategy that doesn’t adapt to volatility can backfire:

Over-withdrawing in bear markets

Missing opportunities in bull markets

Depleting capital too quickly

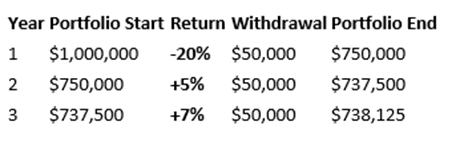

Example: Market Downturn Early vs. Late

Scenario A: Downturn First

Starting Portfolio: $1,000,000

Annual Withdrawal: $50,000

Year 1: –20% return

Year 2: +5%

Year 3: +7%

Figure 1: Scenario A: Market Downturn Early - a Fixed withdrawal strategy locks in losses and reduces the portfolio’s ability to recover in a downturn.

Result:

End of Year 3 Portfolio: ~$738,125

Losses were locked in early

Recovery limited by smaller base

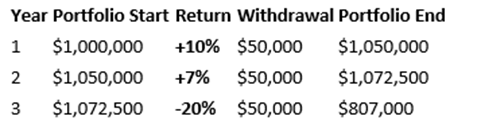

Scenario B: Growth First, Then Downturn

Year 1: +10%

Year 2: +7%

Year 3: –20%

Figure 2: Scenario B: Growth First then Downturn

Result:

End of Year 3 Portfolio: ~$807,000

Early gains created a buffer

Portfolio stayed significantly stronger

How to Protect Your Portfolio with Smart Withdrawal Strategies

Rather than relying on a one-size-fits-all fixed dollar amount, smart withdrawal strategies are dynamic — adapting to market performance and portfolio size. These strategies help you balance income needs with portfolio longevity, reduce risk during downturns, and capture upside during strong years.

There’s no one-size-fits-all solution. The right withdrawal strategy depends on each investor’s unique needs, goals, and the market environment. Below, we outline five proven approaches to help guide the decision:

1 -Percentage-Based Withdrawal

Withdraw a fixed percentage of your portfolio each year (e.g., 4%–5%). Your income will vary depending on market performance, but this approach helps preserve capital during down markets.

Pros:

Automatically adjusts to portfolio size

Helps prevent overspending during downturns

Cons:

Income is inconsistent year to year

Requires flexible budgeting

2- Guardrails Strategy (Guyton-Klinger)

Begin with a target annual withdrawal (e.g., $50,000). Adjust only if the portfolio increases or decreases by 20% or more from its original value. Adjustments are typically ±10%.

Benefits:

Maintains income stability through modest changes

Avoids unnecessary adjustments during minor market moves

Encourages spending discipline in volatile years

3 - Floor and Ceiling Strategy

Define a range for annual withdrawals, only adjusting if your portfolio changes by a set threshold (e.g., ±10%). Adjustments are made gradually, such as ±3% annually.

Advantages:

Smooths out income fluctuations

Provides responsiveness to market changes

Requires careful tracking and rule implementation

4 - Hybrid Strategy

Combine fixed and variable elements to separate essential and discretionary spending:

Use fixed withdrawals or annuities to cover basic living expenses

Withdraw a percentage of your portfolio for discretionary spending

Offers stability for needs while benefiting from growth on wants

5 - The Haghani-White Approach to Retirement Withdrawals

Developed by Victor Haghani (former Salomon Brothers partner and LTCM co-founder) and James White, the Haghani-White approach offers a modern, research-driven alternative to traditional withdrawal rules like the 4% rule. Rather than relying on static assumptions, it emphasizes a dynamic, utility-optimized withdrawal strategy that evolves over time.

Key message:

"You should spend less than you might think early in retirement and adjust dynamically based on outcomes."

Key Concepts in the Haghani-White Model

Dynamic Spending Based on Portfolio Performance

Withdrawals are not fixed. Instead, they should:

Decrease when the portfolio drops in value

Increase when the portfolio performs well

This approach shares similarities with percentage-based and guardrail methods but is grounded in utility theory, balancing spending satisfaction with longevity risk.

Spending Conservatively Early in Retirement

The model warns against overspending in the early years — when portfolios are largest and market outcomes are most uncertain.

Their simulations suggest:

Starting withdrawals around 3%–3.5%, not 4%

Adjusting upward over time as uncertainty decreases

This reduces the risk of depleting assets due to poor early returns (sequence of returns risk).

Incorporating Personal Utility

The Haghani-White framework introduces subjective preferences — asking:

“How much value do I get from spending $1 today vs. in 10 years?”

By weighing the personal utility of money over time, the model allows for more realistic and flexible financial planning than rigid formulas.

Annual “Retirement Spending Update”

Rather than set-and-forget, the model encourages yearly adjustments:

Reassess the portfolio value

Recalculate a sustainable withdrawal

Apply a consumption glide path, where spending changes gradually in line with performance and longevity expectations

How the Methods Compare

Strategy | Flexible? | Market-Responsive? |

| Optimized for Longevity? | Behaviorally Realistic? |

Fixed Withdrawal | ❌ No | ❌ No |

| ❌ No | ❌ No |

Percentage-Based | ✅ Yes | ✅ Yes |

| ✅ Yes | ⚠️ Partially |

Guardrails | ✅ Yes | ✅ Yes |

| ✅ Yes | ✅ Moderate |

Floor & Ceiling | ✅ Yes | ✅ Yes |

| ✅ Yes | ✅ Moderate |

Haghani-White | ✅ Yes | ✅ Yes |

| ✅ Strong | ✅ High |

Summary - Why These Strategies Matter

Adopting a dynamic withdrawal strategy gives you more than flexibility — it gives you control. It allows you to:

🔒 Protect your capital in bear markets

📈 Boost your income in strong market years

🎯 Align your spending with both lifestyle needs and market realities

Withdrawing money from your portfolio isn’t just a financial task — it’s a strategic decision that can determine whether your income lasts 10 years or 30. Rigid withdrawal rules ignore the impact of market volatility, inflation, and sequence-of-returns risk — often with damaging consequences.

Fortunately, modern frameworks such as percentage-based withdrawals, guardrail strategies, and floor/ceiling approaches offer smarter, more adaptive paths. They help your portfolio endure longer and your income remain stable — without sacrificing flexibility.

Among these, the Haghani-White approach stands out for its behavioural and probabilistic foundation. It goes beyond simplicity to offer a scientific, human-centered method for adjusting withdrawals — especially useful in uncertain or volatile environments.

Final Takeaway: Income Is a Strategy, Not Just a Number

A poor withdrawal strategy — particularly a rigid one — can silently erode your wealth and threaten your lifestyle. But a well-designed plan adapts. It accounts for risk. It evolves with your life.

The way you withdraw from your portfolio can have as much impact as how you invested it. Plan wisely — because how you take your income could define how well you live.

Need expert advice on turning your wealth into lasting income? Get in touch — let’s make a plan that works for you.