.jpg)

Why Hedging?

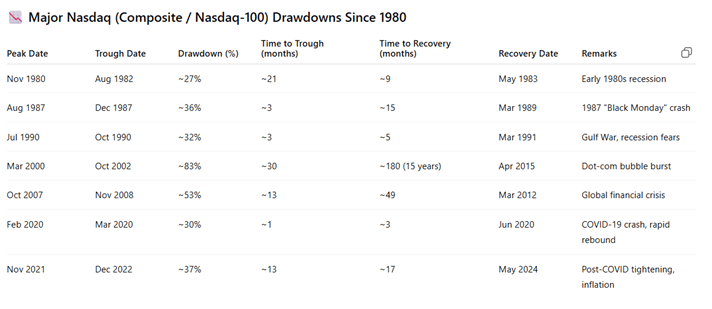

Historically, markets — particularly major equity indices — have demonstrated a strong long-term upward trend. However, they are also prone to sudden crashes and significant drawdowns. Many of these declines have been recovered relatively quickly, often within months or a few years, rewarding patient investors who remain committed and avoid panic selling (see table below).

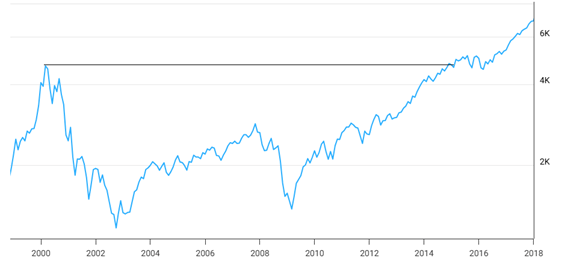

Nevertheless, there have been exceptional periods where recovery has taken much longer. For example, following the bursting of the dot-com bubble in 2000, it took the US Nasdaq index approximately 15 years to fully regain its previous highs.

In the worst case of the last 50 years, between 2000 and 2002, the Nasdaq-100 (NDX) lost over 80% of its value:

Peak: March 2000

Bottom: October 2002

Recovery: April 2015 (over 15 years!)

NDX100 (NASDAQ) Drawdown 2000-2015

If you hold long positions in stocks or ETFs, there are many ways to protect your downside risk. In this article, we concentrate on one of the simplest option hedging strategy: buying put options. Put options are one of the most direct ways to protect your downside risk. A put option increases in value when the underlying asset declines, providing a cushion against market losses.

What are Options?

Options are financial derivatives that give the holder the right, but not the obligation, to buy or sell an underlying asset (such as a stock or ETF) at a specified price (called the strike price) on or before a certain expiration date.

There are two main types:

Call Options: Give you the right to buy an asset at a specified price.

Put Options: Give you the right to sell an asset at a specified price.

Each standard options contract typically controls 100 shares of the underlying stock or ETF. The price you pay to buy the option is called the premium.

Options are used for many purposes: - To speculate on market moves - To generate income - To hedge existing positions.

Understanding Options and Volatility: The House Insurance Example

Volatility is a key concept in options pricing and can be roughly described as risk — the likelihood of large, unexpected moves in the price of an asset. To understand this better, think of options as a form of “insurance” for your investments.

Imagine you own a house. If your house is located in a safe, stable area, there is a low chance of extreme events (like floods, earthquakes, or fires). In this case, the volatility (risk) is low, so your insurance premium is relatively inexpensive.

On the other hand, if your house is built in an earthquake-prone zone, the risk of a disaster is much higher. Here, the volatility is high, and therefore, the insurance company will charge you a much higher premium to cover this greater risk.

Options as financial insurance

When you buy a put option, you are essentially purchasing insurance against adverse price movements. A put option protects you from a drop in the value of your asset, just like home insurance protects you from property damage.

The price of this "insurance" (called the option premium) depends on many factors - one of the most important is volatility. If the market expects bigger swings (high volatility), options become more expensive, just as home insurance becomes costly in high-risk zones.

Timing matters

The best time to buy home insurance is before a disaster strikes, when the risk is perceived to be low and premiums are cheaper. Similarly, the best time to buy options to hedge your portfolio is during periods of market calm, when volatility is low and premiums are more affordable.

Waiting until after a market shock (or an "earthquake") usually means paying much higher prices and protection can become unaffordable.

The Cost of Options: What You Really Pay

The cost of an option is called the premium, and it’s influenced by several factors, among which:

Time to expiration (longer = more expensive): the longer the period you ensure for, the more expensive is the option.

Implied volatility (higher = more expensive): the more the risk, the more expensive is the option.

Distance from strike price: the more the “amount” ensured, the more you pay for the option. Ensuring against a market fall of 5% or more is going to be more expensive than ensuring only falls more than 30%.

Benefits of Hedging with Buying Puts:

Capital Protection: Functions like insurance, providing a safety net against steep market declines.

Maintain Upside: Unlike stop-loss orders, put options allow you to stay invested and benefit from potential market rebounds without triggering unwanted sales.

Defined Risk: our maximum loss is limited to the premium paid if the market continues to rise — providing clarity and peace of mind.

Cons of Hedging with Puts:

Cost (Premium Paid): The option premium represents a real cost and will reduce your portfolio’s overall return, especially if the hedge isn’t needed.

Limited Duration: Like insurance, protection is only valid for a specific period. Once expired, you must renew or "roll" the hedge to maintain coverage.

Complexity and Non-Linearity: Options are not straightforward; their value before expiration depends on multiple factors (volatility, time decay, underlying price), and protection is fully realized only at or near expiration.

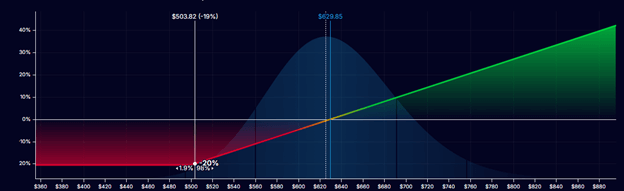

Example: S&P 500 Tail Risk Protection

In a real-world scenario, in July 2025 we can ensure our S&P 500 U.S. stock market exposure against a 20% decline or greater over a 6-month period for a cost of approximately 0.65% (or roughly 1.3% annualized).

This kind of long-dated protective put strategy offers portfolio insurance at a low cost. The graphic below shows the potential outcomes:

S&P 500 Drawdown Hedge

At a 20% drop or more, the protective put begins to offer strong positive returns, capping the portfolio drawdown at expiration.

If the market remains stable or rallies, the cost is capped to just the cost, the premium paid, and you can still benefit from market appreciation.

This illustrates how even modest allocations to options can provide significant protection during rare but severe downturns.

Why Options Aren’t for Everyone

Options are powerful tools, but they’re not suitable for every investor.

Key Reasons:

Complexity – they seem deceptively simple but, in reality require knowledge of complex aspects such as time decay, volatility, delta, gamma, etc.

Leverage – options are risky and leveraged instruments → gains/losses can be greatly magnified. You can lose a lot of money very quickly if you don’t know what you are doing.

Time Decay – Options lose value as they near expiration, even if your view is right but you are early.

Execution Risk – Illiquid options can be hard to enter/exit at fair prices

Emotional Stress – Options trading demands timing, discipline, and fast decision-making

Tax and Compliance Complexity – May trigger short-term gains and regulatory scrutiny

Why Options Are Simple in Theory — But Complex in Practice

At first glance, options appear straightforward: they give you the right, but not the obligation, to buy or sell an asset at a certain price within a specific time. Many investors think of them as easy, flexible insurance.

But, in reality, options are highly sophisticated instruments whose value depends on multiple moving parts: volatility, time decay, market direction, interest rates, and more. The complexity isn’t just in pricing — it lies in all the decisions you must make:

When should you hedge?

How much should you hedge (declines of more than 5%, 10%, 20% or 50%)?

What cost is reasonable?

What is the best moment to hedge?

How long should your hedge last?

Which instruments should you use?

These choices may seem simple but are far from trivial in practice. Answering these questions requires a deep understanding of option theory and of your portfolio, risk tolerance, market conditions, and objectives.

Options are complex and volatile instruments that should only be used by investors who thoroughly understand their risks.

Conclusion: Options as a Strategic Tool

Options can be an efficient and flexible way to protect, leverage, or generate income — but only if used with the right knowledge and intention. For investors and portfolio managers, especially those running long-only ETF and stock strategies, put options can serve as invaluable tools for managing risk without sacrificing long-term growth.

However, understanding the true exposure, cost dynamics, and when and how to hedge is critical. Used responsibly, options can help you navigate volatility and build more resilient portfolios for the future. If used incorrectly, options can introduce unnecessary risks and additional costs to your portfolio.

And always remember: you hedge when you can, not when you need to. Insurance becomes prohibitively expensive in a market crash.

Interested in a hedging consultation or custom option strategy? Contact our team for a tailored risk analysis.